12 May, 2021 Emerging markets indicate preference for contemporary sustainability frameworks, finds GlobalData

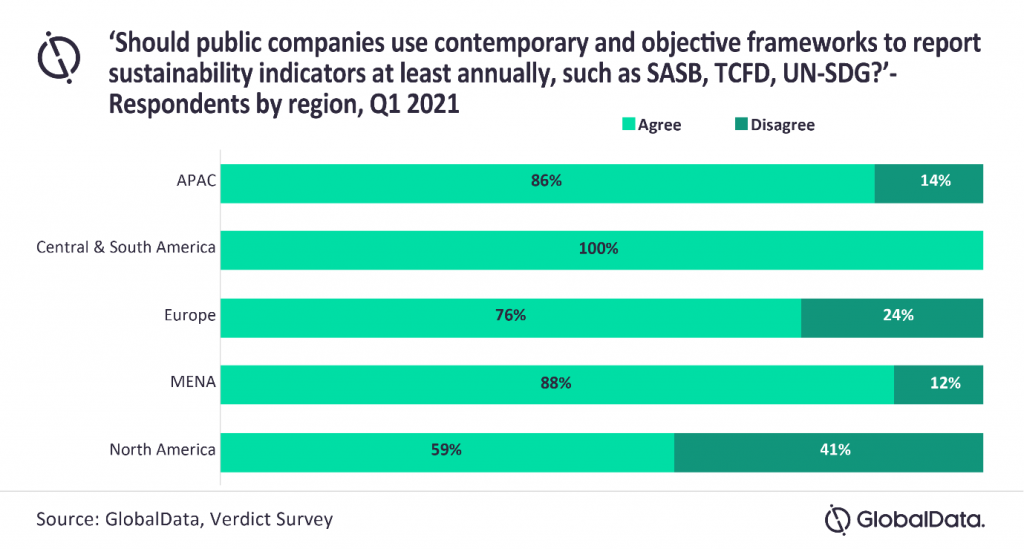

Posted in Business FundamentalsThe Q1 2021 Verdict survey* by GlobalData, conducted to assess the perception around sustainability reporting, found that 74% of respondents voted in favour of public companies using objective and contemporary frameworks. Examples of these framework types include the Sustainability Accounting Standards Board (SASB), the Task Force on Climate-related Financial Disclosures (TCFD) and the United Nations’ Sustainable Development Goals (UN-SDG) for sustainability reporting. Geographic classification of the poll’s statistics revealed that India had the highest proportion of respondents (93%) favouring contemporary frameworks, while the US had the least at 58%.

Sourish Chatterjee, Principal ESG Analyst at GlobalData, comments: “The value of sustainability reporting is multifold. At the outset, it facilitates consideration of environmental, social, and corporate governance (ESG) impact across products, services and operations while also enhancing transparency around ESG risks and opportunities. This transparency translates into heightened information symmetry for investors, highlighting the preference for novel frameworks.”

At a broader level, all respondents from Central and South American geographies favoured contemporary frameworks, followed by the MENA and APAC regions, with 88% and 86% of the respondents in favour of contemporary frameworks, respectively. In contrast, only 76% of the respondents in Europe, and 59% of the respondents in North America, favoured contemporary frameworks.

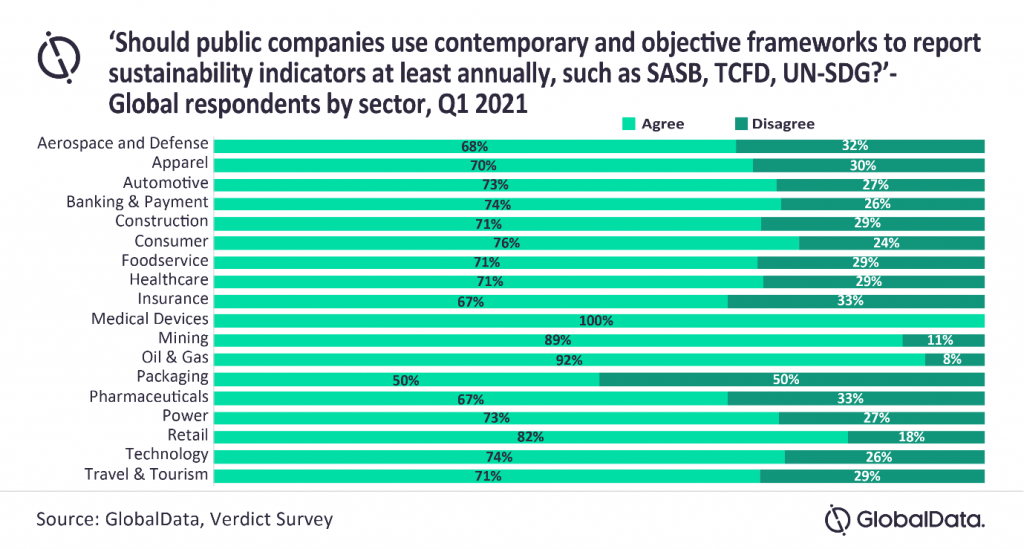

By industry, the medical devices sector was the only one to see all respondents favouring contemporary frameworks.

Chatterjee continued: “Emerging markets must comprehend and leverage competitive advantages that can be derived from effective sustainability strategies. Transparency and reporting can provide substantial opportunities to companies seeking investments in markets generally characterized by lack of material information, especially regarding sustainability.

“While most companies in developed markets have traditionally used the global reporting initiative (GRI), the adoption of SASB and TCFD is a growing trend in these markets. The surge in adoption of such contemporary frameworks is likely due to investors being hungry for information on how ESG impacts a company’s financial performance.”

The SASB facilitates reporting and analysis of the financial impact of sustainability, allowing both investors and companies to report and analyse sustainability from a financially relevant standpoint. Similarly, The Financial Stability Board created the TCFD to improve and increase reporting of climate-related financial information.

Chatterjee concludes: “SASB’s granularity is a key difference compared to conventional frameworks such as GRI. Its focus on the financial impact of sustainability causes it to be important to investors, debt holders and internal stakeholders. TCFD’s framework is built on the need for financial markets to assess the impacts of climate change, inclusive of managing the risks and opportunities associated with emerging clean technologies.

“It is important for ESG disclosures and the resulting analysis to facilitate actionability and readability of data, in order to generate reliable signals and increase the effectiveness of associated capital investments. In 2020, the SASB, GRI and others focused on creating a universal consensus for better clarity. Uniformity and clarity in reporting practices is an objective for all stakeholders, set to create a profound impact on the information and regulatory landscape.”

*GlobalData’s Verdict survey based on 420+ responses from respondents across the globe